Bond yield and investing

During the last calendar quarter of the year 2021, the interest rates started turning, with the benchmark Bond Yield (10 Y) threatening to breach 6.5%, and which it finally did. Presently the 10 Y Yield is around 7.4%, after having crossed the 7.5% mark in the first week of June 2022, first time after March 2019. Primarily, a rise in the yields has been brought about by a surge in the global oil prices, high inflation and due to aggressive government borrowing program.

Globally, the rising inflationary trend has compelled the central bankers to raise interest rates and with it the Yields have been moving higher. In fact, the RBI unexpectedly raised the key repo rate, on 4th of May, first time since 2018, by 40 bps to 4.4%, due to inflation staying above its 2% to 6% tolerance limit (at 6.95%) for the third month in a row. Inflation has breached the 7% mark since then (having touched the 7.8% mark in April 2022) and has stayed there and resultantly the Repo rate was further increased by additional 50 bps and stands at 4.9%.

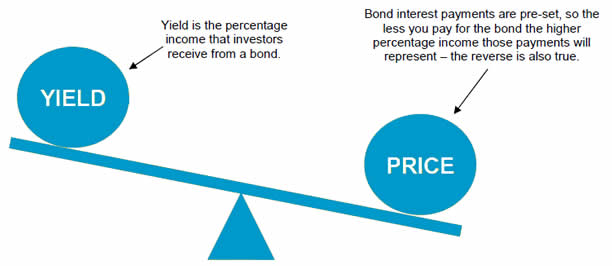

Investors track Bond Yield closely because there is an inverse relationship between a bond and its yield – when a bond’s yield rises, its price falls. Therefore, rising yields are leading to a correction in the Bond market, leaving investors with mark-to-market losses. Higher the maturity of the bond the greater the fall in its price due to a rise in yields.

Banks get impacted by the yield movement, as well. Since the banks maintain large holdings of government securities, including State Development Loans (SDLs) and treasury bills, as part of regulatory investment requirements, any hike in the yields results in a fall in the bond prices, leading to mark-to-market losses (also called Treasury losses). In fact, as per an ICRA report, Banks are likely to report mark-to-market losses of up to Rs.13,000 crore on their investment portfolios in the April-June quarter.

:max_bytes(150000):strip_icc():format(webp)/what-economic-factors-influence-corporate-bond-yields_final-fb307b0178404442a1cf7fd2a4d4db06.png)

For Equity investors the bond yield is an important metric. This is because a widening gap between the bond yield and earnings yield (which is the inverse of the price-to-earnings ratio or PE ratio) makes it less attractive to stay into equities. For instance, in the first week of June 2022, when the 10Y yield breached 7.5%, the Nifty earnings yield was at 4.88%. As a result the yield gap was 2.62%, up from 1.97% in February 2022. This has enhanced the appeal for debt instruments over equities. Although on a standalone basis, the earnings yield appears attractive but the rising bond yield is making it seem less attractive.

For Borrowers too, the movement in Yields is of immense significance. Since higher yields imply costlier borrowing costs, the two biggest borrowers in the country – government and corporates – are adversely impacted due to rising yields.

Rising bond yield impacts investors and borrowers adversely. Also, the extent of impact depends on the longevity of the trend and on the quantum of rise.

Table of Contents