The most important thing to learn in investing is compounding!

“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it”, was likely remarked by the legendary Albert Einstein. In real life though, while quite a few investors do (understand and know about compounding) but are unable to fathom the deep impact it (compounding) could have on one’s wealth, over a period of time. Would like to share an interesting example to illustrate this point.

If you were receive a sum of money after 30 days, which option would you choose?

- Rs.5 crores in one go.

- Rs.1 on the first day and doubling it every day for the next 30 days (i.e. incremental Rs.2 on the second day, Rs.4 on the third, Rs.8 on the fourth and so on)

Intuitively, most would go with the first option, of Rs.5 crores in lumpsum, even when in the second option doubling Rs.1, every single day over the next 30 days will yield a mammoth Rs.53 crores – 10 times more than the lumpsum option. Such is the magic of compounding. One reason why most investors disregard the impact of compounding is because the human brain generally works on arithmetic (simple) growth and not geometric (compounded) growth.

Theoretically speaking, compound interest is the interest you earn on interest. It arises when interest is added to the principal such that the interest added also earns interest. This addition of interest to the principal is called compounding. Herein, an important parameter is ‘time’ – the more time that an investment has to compound, the greater the potential return will be. In fact, compounding is the impact of ‘time value’ of money over multiple periods into the future.

The key elements of time value of money are:

1) Number of time periods, say years

2) Annual rate of return or interest rate

3) Present value (the invested amount, could be staggered or lumpsum)

Clearly, as an investor you exercise varying influence on each of these elements. What you could invest periodically is a function of your income and investible surplus available with you. The rate of return shall be a factor of your risk-taking ability and your asset allocation (composition of your portfolio across equity, debt, gold, alternatives, cash). Investment horizon could be a function of your age, life-stage and/ or financial goals. Nonetheless, by starting early, investing consistently (in sync with one’s risk profile and returns expectations) and by staying invested over a long period of time you could reap the benefits of compounding.

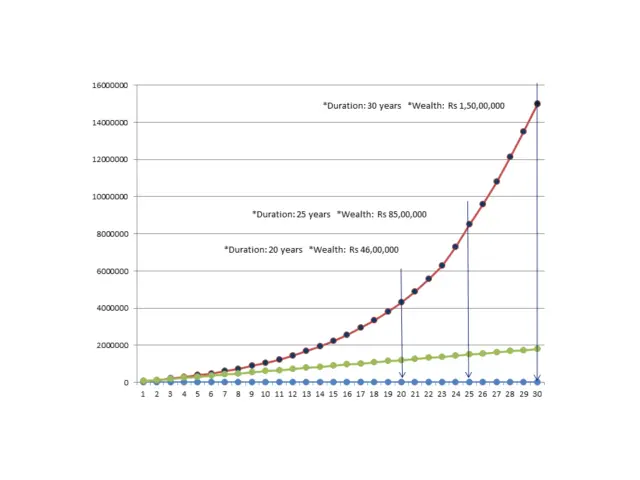

An investor compounding his/ her wealth at 8% pa shall double the investment every 9 years whereas one compounding at 15% pa will do so in every 5 years. Not only that, over a 25 year period, the investor compounding at 15% pa will end up with almost 5 times more wealth than the former (other things being equal).

The question is: at what rate are you compounding yours?

Ref: Investopedia

Table of Contents