Stick to your asset allocation, minimise cost of investing and have an investor mindset

While investing through managed portfolios, like Mutual Funds, Portfolio Management Service (PMS), Alternative Investment Funds (AIFs), Structures Products, Market-Linked Debentures (MLDs), and lately even Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InvITs), an investor exercises control on only three, but highly critical, parameters while making a investing choice:

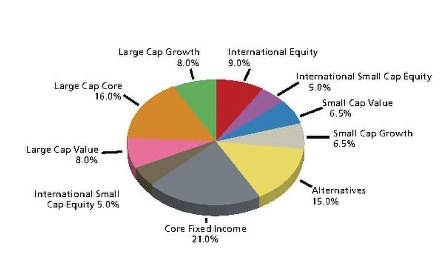

A) Asset allocation

Asset allocation is the single largest determinant of portfolio performance, contributing about 90% of the portfolio returns (as per various studies). Simply put, asset allocation is the allocation of investible surplus across asset classes like Equities, Bonds, and Alternatives (Real, Estate, Bullion, Commodities) with the ultimate aim of balancing risk and reward.

Each asset class has a risk profile which is distinct from others. For instance, while Equity offers growth but is volatile, debt has the potential to counter portfolio volatility, while ensuring stability. Alternatives (like real estate) have the potential to provide regular income but are illiquid. The interplay of various asset classes, residing inside an investor’s portfolio, engenders risk mitigation and optimises returns, over a long p

An ideal asset allocation is arrived at by assessing one’s risk tolerance, financial goals, and time horizon. Especially, once an investor has generated significant wealth, it is advisable to determine his/ her risk-reward expectations and to make relevant changes to the portfolio accordingly. This needs to be repeated at regular intervals (of say 3-5 years) ensuring alignment with one’s risk profile, then.

B) Cost of investing

The second parameter, Cost (of investing), usually, does not get its due importance while evaluating an investment opportunity. Although the regulatory mechanism has made way for commission-free investment options to the investors, but very few are aware of this. Most seem to be oblivious of the fact that a small difference in the recurring expense ratio, of a fund, could reduce the returns significantly, over a period of 3-5 years.

A fee expressed as a percentage doesn’t reveal to an investor the amount being spent toward expenses and its impact on the corpus. For instance, an investment of Rs.1 crore in a combination of well-diversified mutual funds would have saved an investor Rs.13.8 lakhs by merely investing through the Direct plan (as against Regular plans), over 5 years (data as of 31st May’21) – a return differential of 13.8% with the same risk level.

C) Time in the market

“Time” in the market, by far, is the single most critical factor influencing the end returns. What it simply means is that instead of trying to second guess the market highs or lows, the investor should stay with the market, ‘participating’ in the businesses/ sectors held as the business cycles play out over 3-5 years (or even longer) periods.

The ‘time-in-the-market’ strategy helps in getting rid of the trader/ speculator mindset of relying on the market ‘noise’ and instead lets a long-term investor focus on one’s risk profile and stick to one’s suggested asset allocation.

Proactive use of these three levers helps an investor in not only optimising the end-returns but also help mitigate the attendant risks – the two most critical outcomes in investing.

Table of Contents